Every quarter, the Flex Index holds up a mirror to how companies are navigating the future of work. This quarter’s data makes one thing crystal clear: flexibility is not going away. It is still the center of gravity for how modern organizations operate.

From the world’s biggest enterprises to the smallest firms fueling employment growth, the story is consistent: flexibility is not just an employee perk. It is a business performance driver.

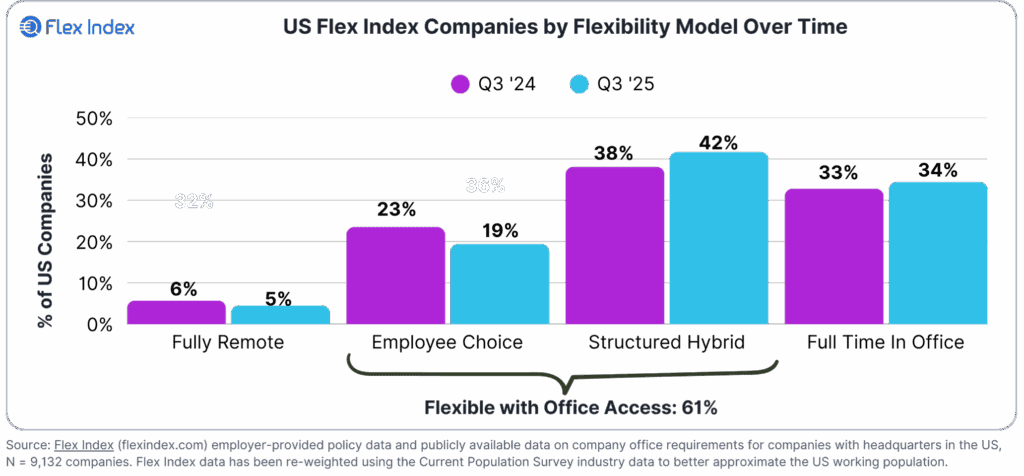

Flexibility Is Still the Norm

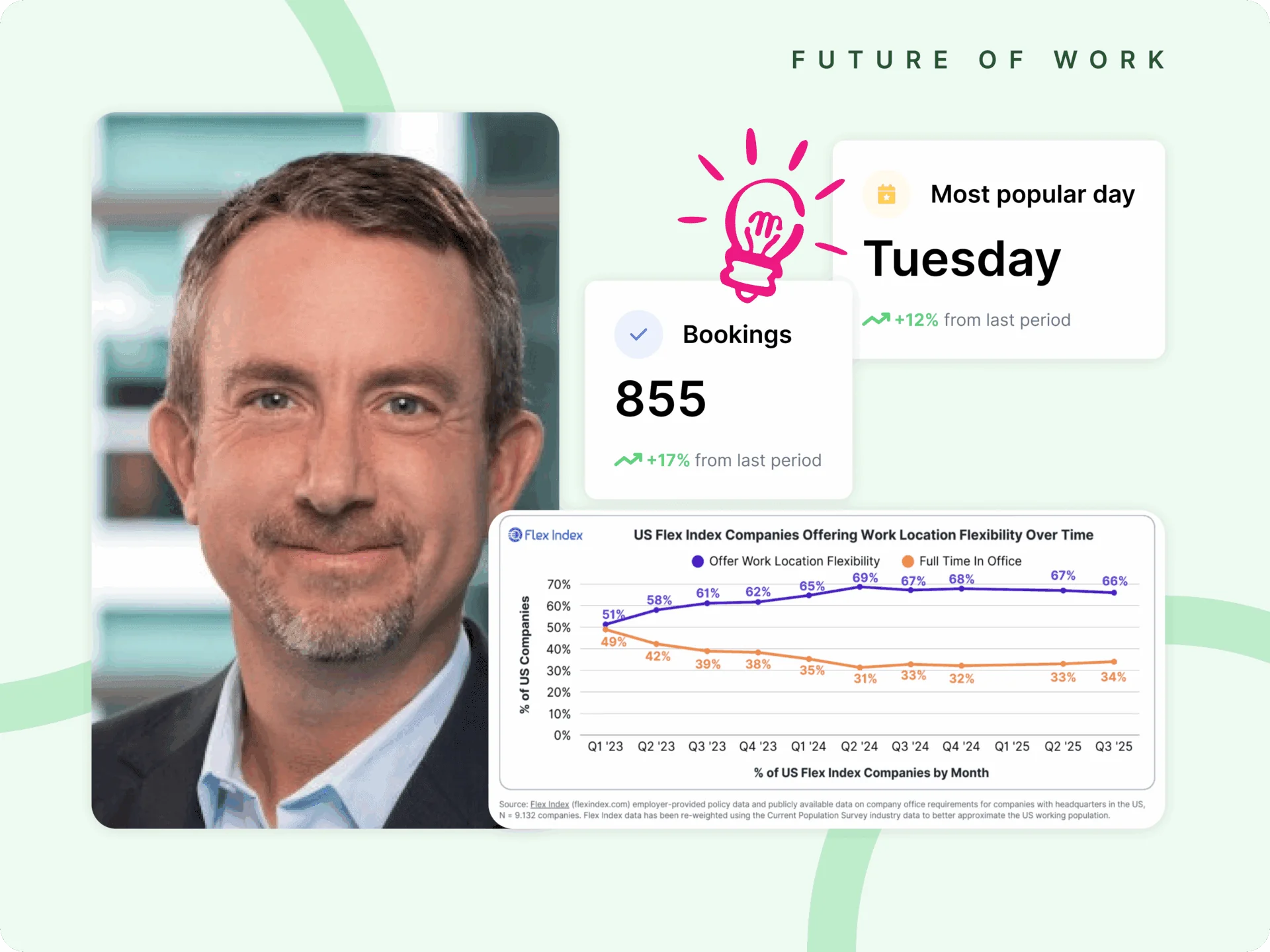

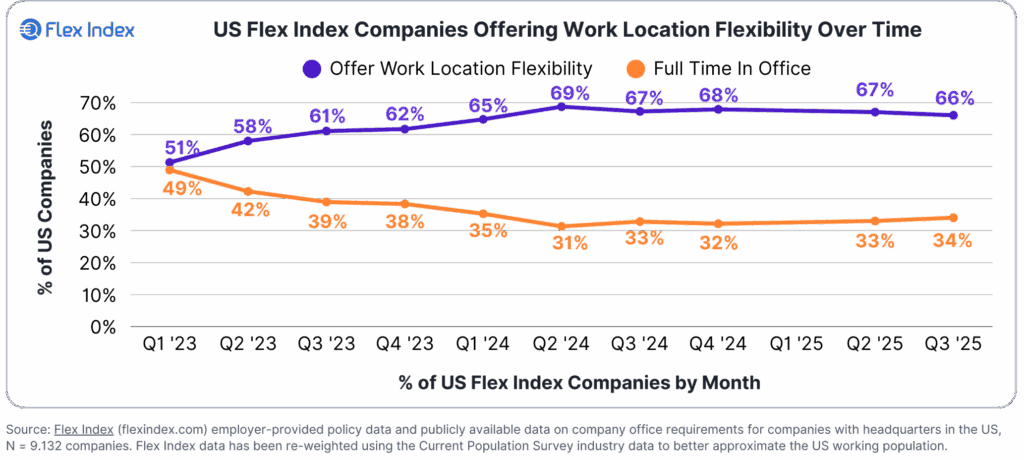

Despite headlines about mandates, two-thirds of U.S. firms continue to offer location flexibility. Only a third require full-time office presence, and the uptick from last year was small and driven mostly by government agencies.

For leaders, this tells us something important. Even as some sectors tighten their grip, the market overall is moving toward balance, not retreat. Employees expect flexibility, and most companies are finding ways to deliver it.

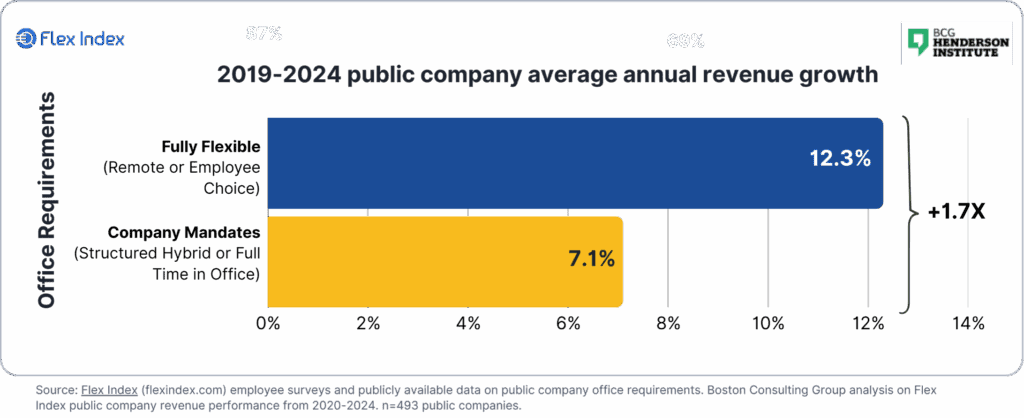

Flexibility Drives Performance

The data is undeniable. Fully Flexible firms grew revenues 1.7 times faster than mandate-driven peers between 2019 and 2024. Even when adjusting for industry and company size, the growth advantage holds at 1.3x.

This is not just about employee satisfaction. Flexibility shows up in the numbers. When people have more control over where and how they work, businesses move faster, attract better talent, and retain the teams that drive results.

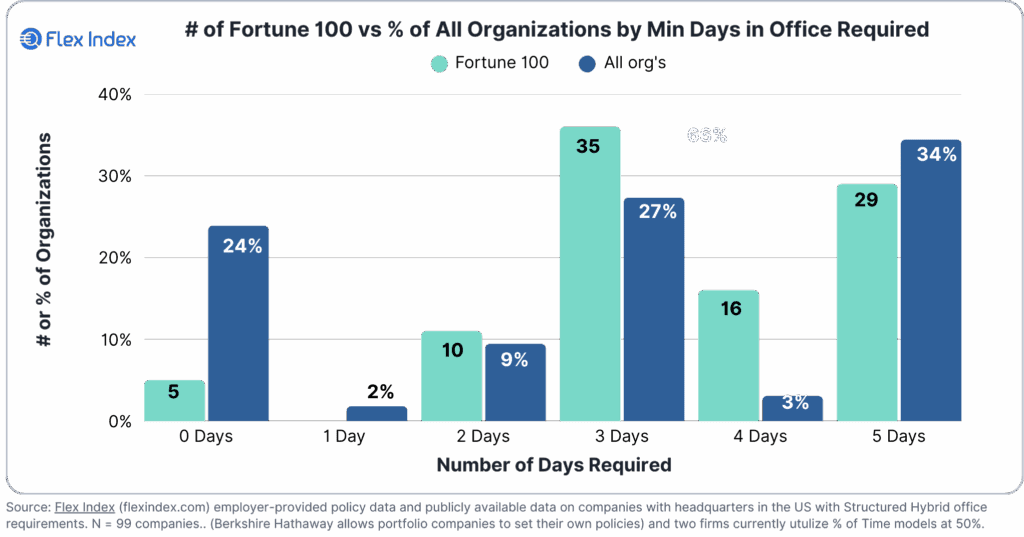

The Fortune 100 Tightens But Does Not Break

Among the Fortune 100, flexibility is still the default. Seventy-one percent remain flexible, with three-day hybrid as the most common policy. But the shift is clear: nearly half now require four or five days in office, signaling a tilt toward stronger mandates.

It is worth watching. These are companies with huge brand power, but they are also competing with smaller firms that can outmaneuver them on talent by offering greater freedom.

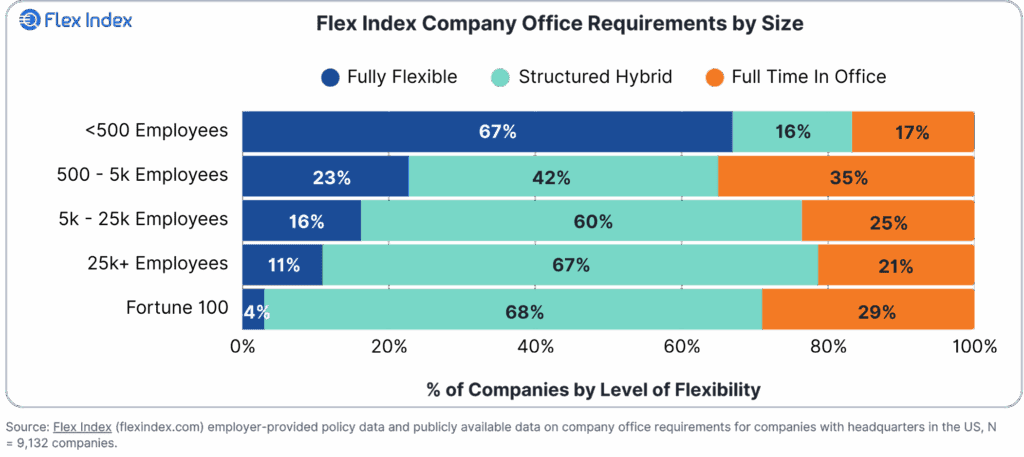

Smaller Firms Hold the Advantage

The contrast is striking. Two-thirds of companies with under 500 employees are Fully Flexible, covering half the U.S. workforce. That flexibility is translating into real momentum. Smaller firms are responsible for nearly all net employment growth in the country.

This divide matters. Employees know where to find flexibility, and increasingly that is in smaller, nimbler organizations.

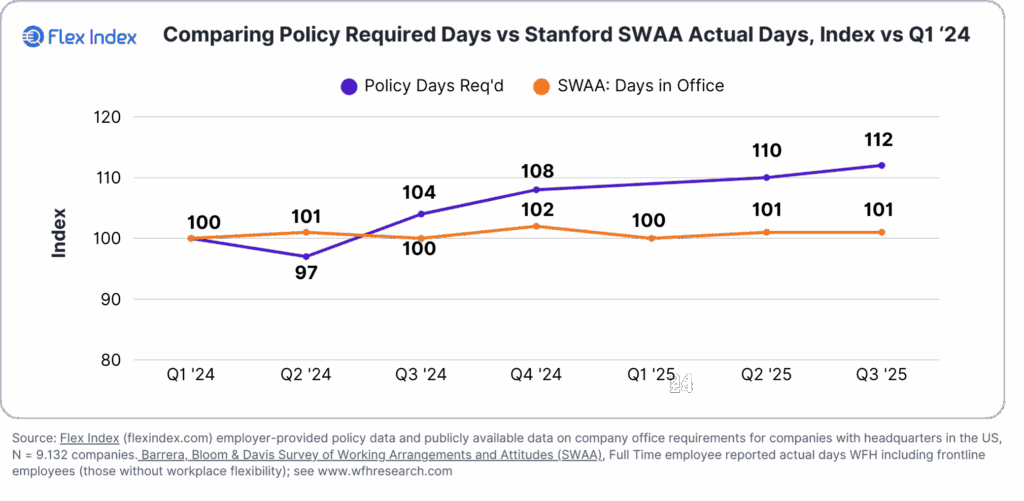

The Compliance Gap Persists

Perhaps the most telling finding this quarter is the widening gap between policy and behavior. Required office time is up 12 percent since early 2024, but attendance has only risen by 1 to 3 percent.

This is the heart of the debate. You can mandate attendance, but that does not mean people will comply or that performance improves when they do. Leaders need to ask: what are we really trying to achieve? Forcing people into a building is not the same as building culture, engagement, or productivity.

Flexibility Shapes the Future of Offices

Finally, let us talk about the office itself. The majority of firms are not abandoning offices. They are redefining their purpose. Sixty-one percent now offer both flexibility and access to space. Offices are becoming hubs for connection, collaboration, and identity, not compulsory nine-to-five enclosures.

The smart office of the future is not about filling seats. It is about enabling people to do their best work, wherever that happens.

My Takeaway

Flexibility is no longer the question. It is the answer. The debate over whether hybrid has “won” is behind us. The real challenge now is how organizations will harness flexibility to drive performance, attract talent, and make their spaces matter.

The companies that understand this, whether they are 500 people or 50,000, will be the ones who thrive in the decade ahead.

Join us in this webinar on September 16 (Tues) for a discussion co-hosted by Flex Index and Kadence, exploring how enterprise leaders can navigate the widening gap between policy and behavior, and what strategies will define the future of work – reserve your spot here