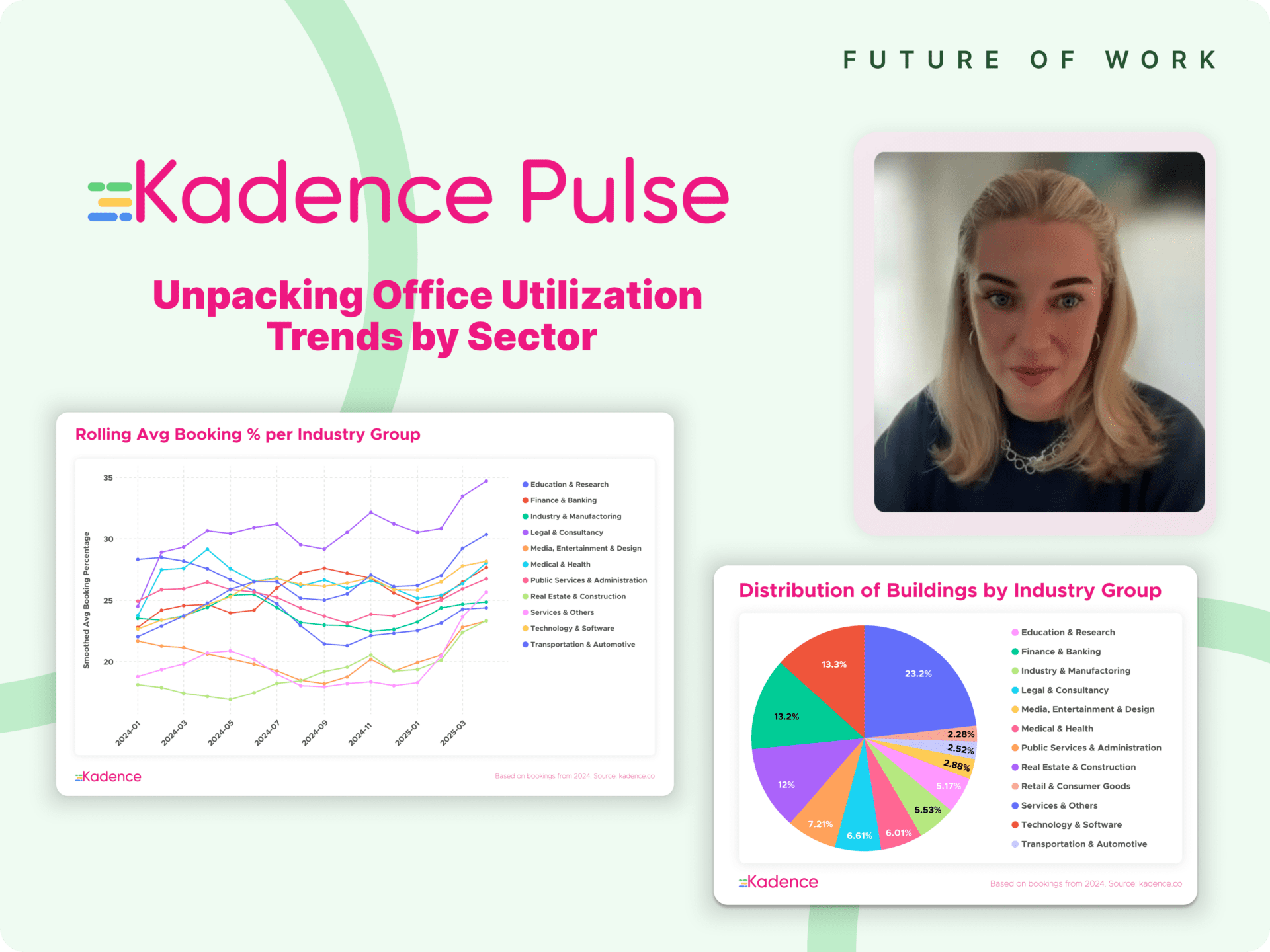

Welcome to Kadence Pulse, our deep dive into how hybrid work is evolving—powered by real-time desk booking data from our customers using Kadence.

After a year of settling into hybrid rhythms, the first half of 2025 is showing signs of structural change in how different sectors are using office space. Our latest analysis — drawn from over 1,100 office buildings between January 2024 and May 2025 — reveals not just a rebound, but a divergence.

Some industries are going all-in on the office. Others are still circling the block.

Let’s get into it.

A Quiet Majority, A Loud Few

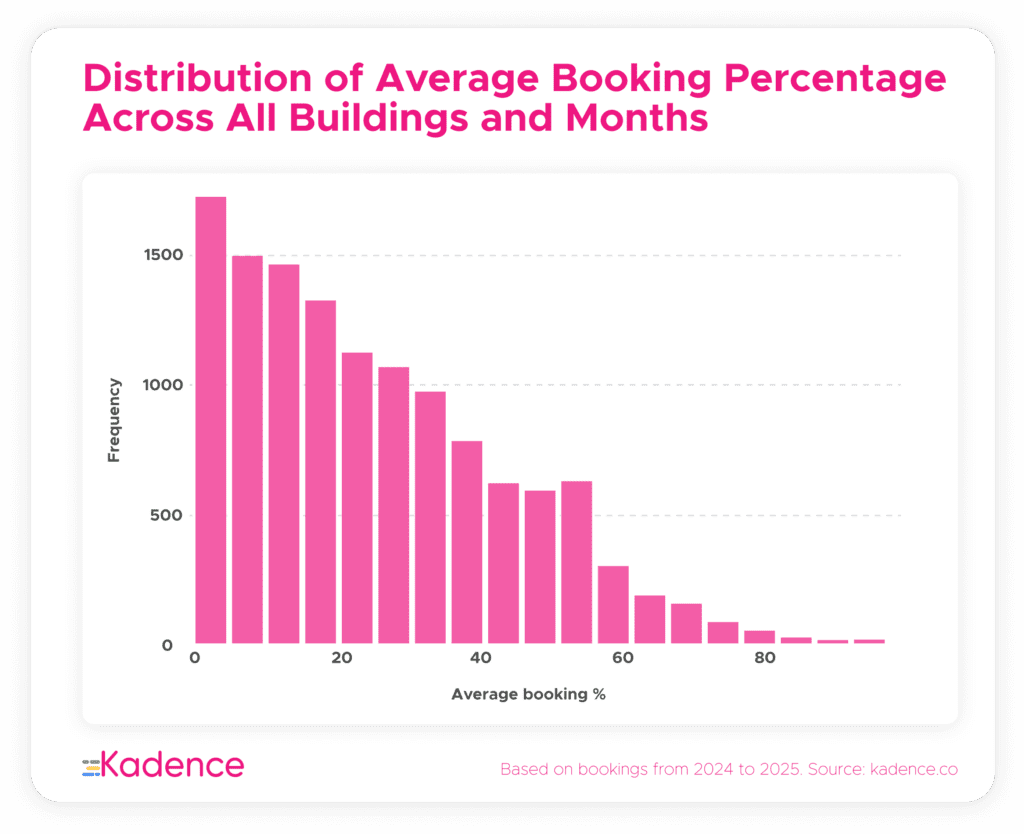

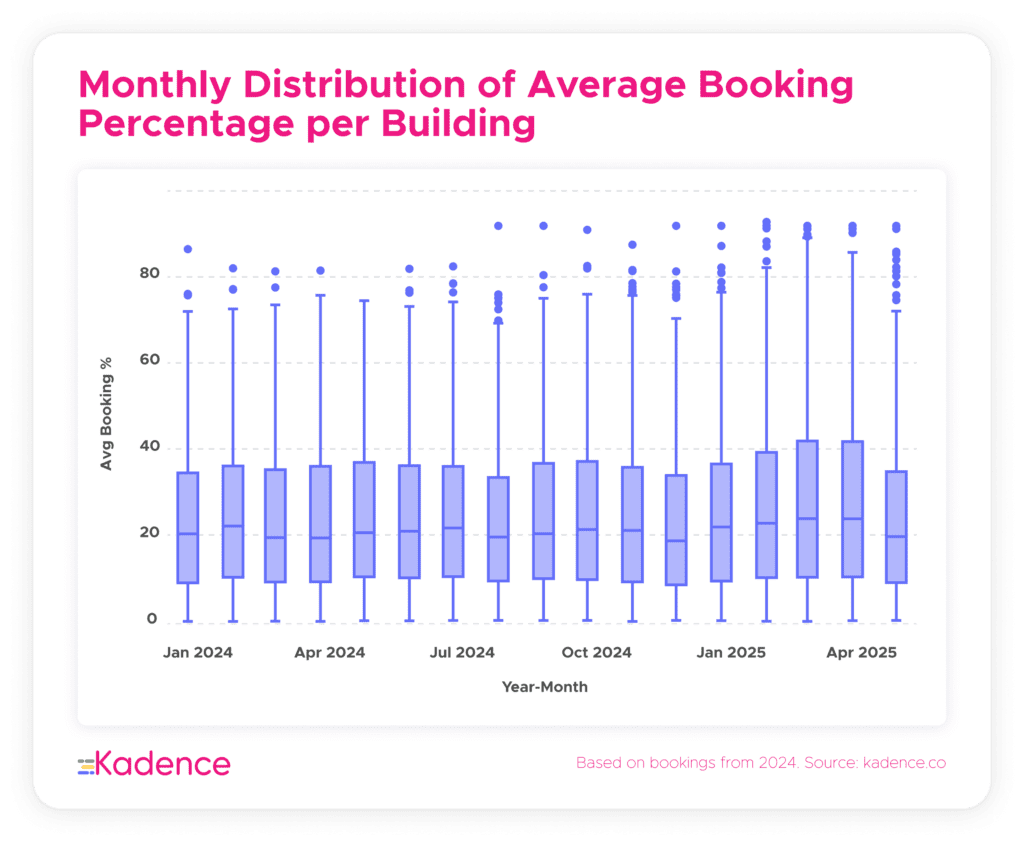

Across the board, most offices are still running cold. Average desk utilisation remains concentrated in the 20–40% range, with few buildings pushing beyond that threshold.

But outliers are getting louder.

Since November 2024, we’ve observed an increase in buildings hitting or exceeding 80% monthly utilisation. That tail of high performers is lengthening — suggesting that some tenants, perhaps entire sectors, are beginning to double down on the office.

The distribution hasn’t just shifted — it’s splintered.

Benchmarking Kadence Trends Against Industry Data

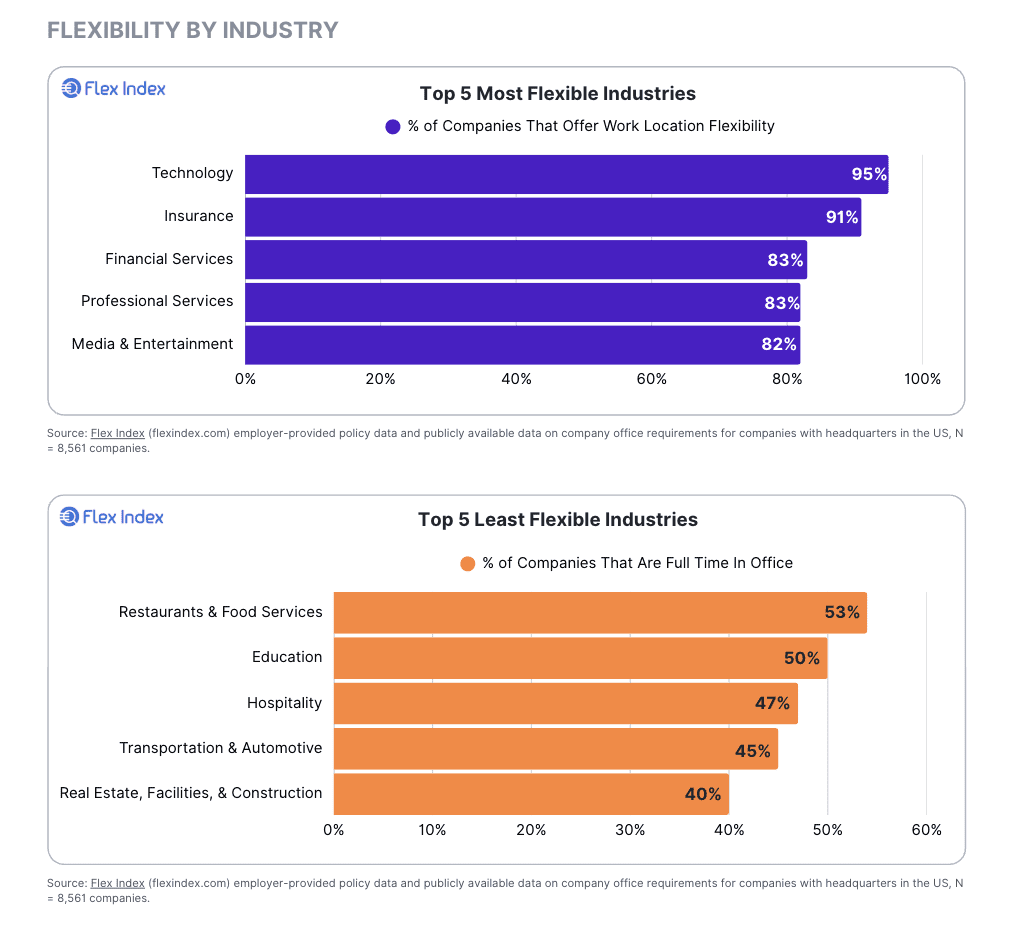

To understand how Kadence customers compare to broader workplace trends, we benchmark our internal data against two leading industry sources: CBRE’s space utilization figures and Brian Elliott’s Flex Index on workplace flexibility.

According to CBRE’s 2024-25 workplace study, average space utilization across industries remains relatively low, with a cross-sector average of just 38%. Sector-specific breakdowns show:

- Life Sciences: 48%

- Financial & Professional Services: 40%

- Industrial & Logistics: 39%

- Technology, Media & Telecommunications: 35%

- Other: 26%

These utilization rates are strikingly similar to what we see across Kadence’s customer base — suggesting that our users mirror global norms in how office space is being used.

But the difference lies in the detail. Where CBRE offers a top-down occupancy snapshot, Kadence tracks behavior in real time — surfacing midweek peaks, sectoral outliers, and early signs of cultural alignment.

And when we add a third lens — the Flex Index, which tracks how many companies allow flexible work — the story gets even more compelling.

- 95% of technology companies, and over 80% of financial and professional services firms, offer location flexibility.

- These same sectors rank highest in Kadence’s real-time utilization data — not just showing up, but doing so in concentrated, coordinated ways.

- Conversely, real estate and transportation, which the Flex Index flags as least flexible, lag behind in Kadence utilization as well — despite often requiring full-time attendance.

The implication? Flexible-first industries aren’t avoiding the office — they’re making smarter, more purposeful use of it. It’s not just about policy. It’s about rhythm, intent, and making the office worth the commute.

Kadence gives teams the signal intelligence to do just that — not only to align their space with demand, but to adapt it to how their people actually work.

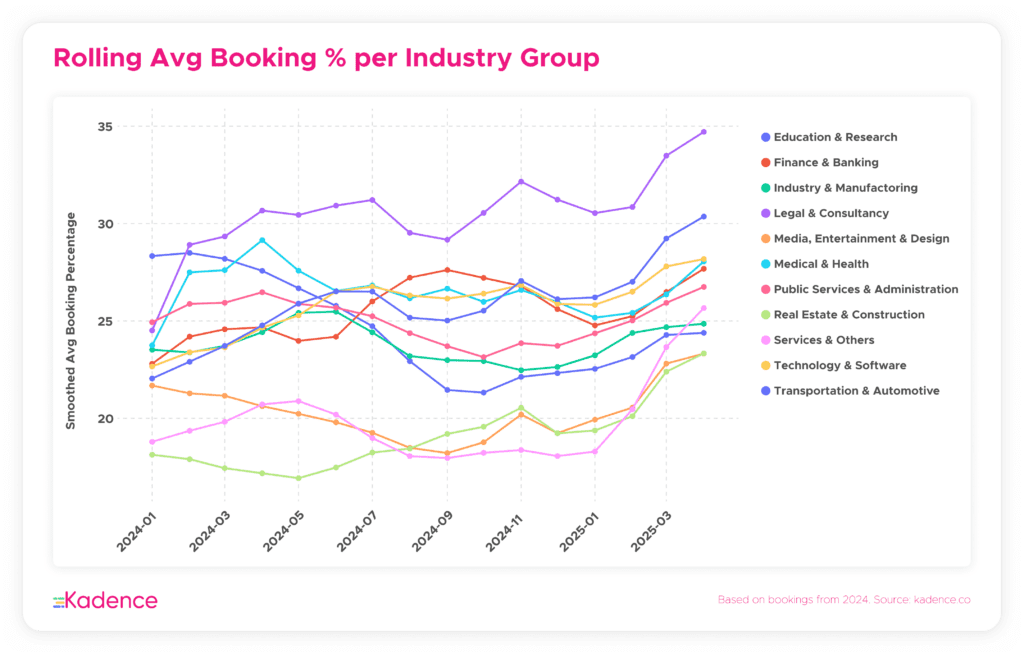

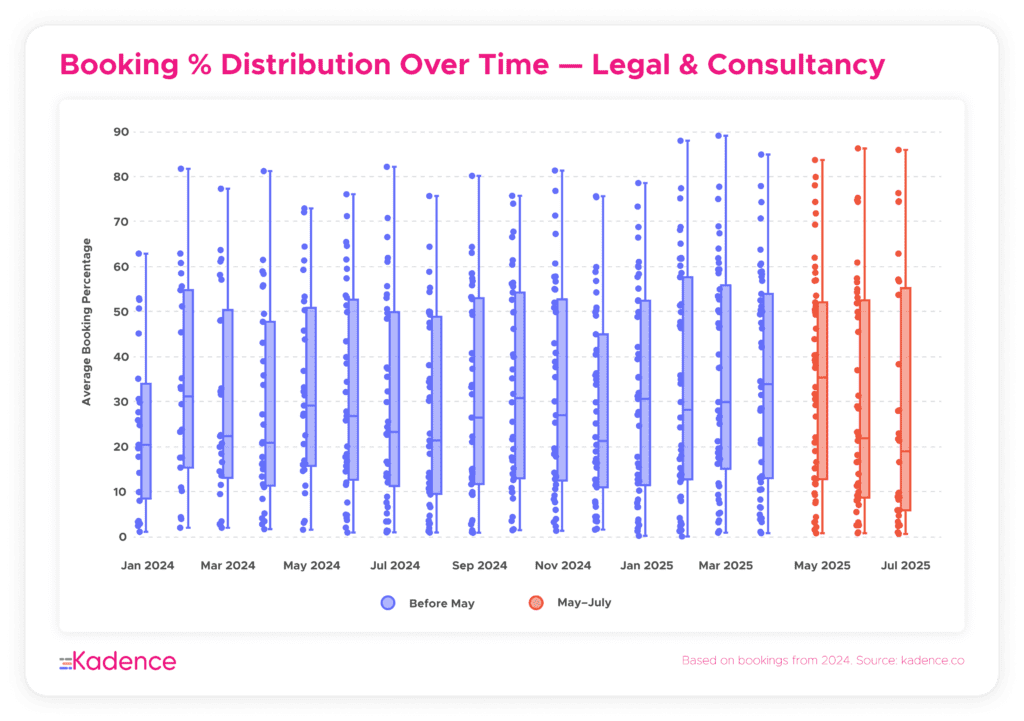

Legal & Consulting: Steady, Strong, And Surging

No sector shows more intent than Legal and Consulting. These firms not only have the highest average utilisation, but also the widest range — meaning their use of space varies dramatically across locations, but at the top end, it’s thriving.

- The upper quartile of legal buildings hit 50%+ utilisation.

- A steady month-on-month increase began in January 2025, with no sign of slowing.

- Even the Christmas dip was smaller than other sectors.

This goes beyond mere attendance. It’s about alignment. Legal teams are notably committed to in-office collaboration due to longstanding cultural norms that emphasize mentorship and client interaction, the competitive edge of face time in high-margin, client-facing work, and the influence of senior leaders who often favor an office-centric culture.

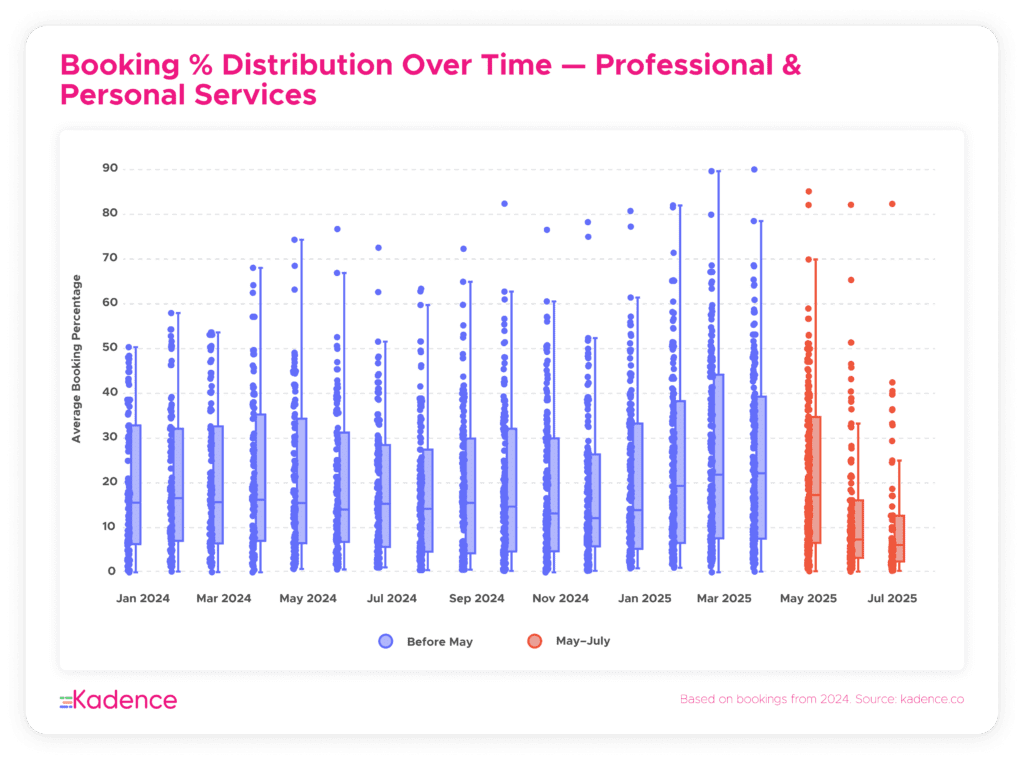

Professional & Personal Services: Spiky But Rising

The Professional & Personal Services sector — a broad bucket — is showing some of the most dramatic surges.

- From February to April 2025, some buildings hit 90%+ utilisation.

- The tails have lengthened, suggesting not just isolated peaks but a spread of higher in-office engagement.

- Average usage climbed sharply in Q1 2025.

This might reflect companies in this group leaning harder into team-based work — or being pushed by client expectations. A preference for in-person mentorship, secure client engagement, and a culture shaped by senior partners means these firms continue to value the office as a competitive advantage.

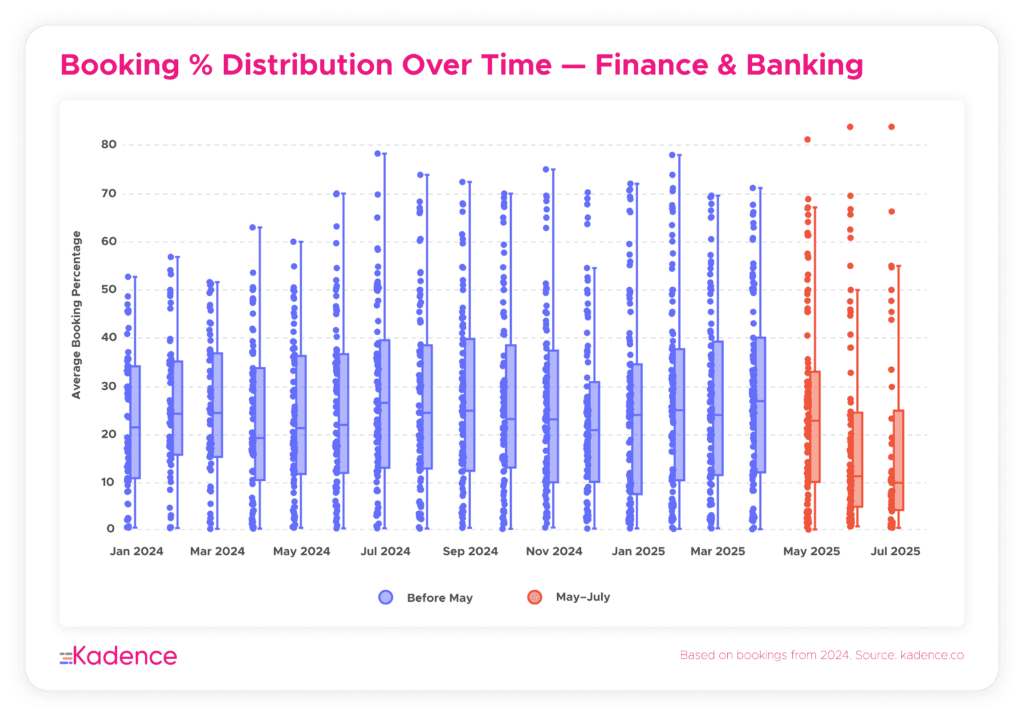

Finance & Banking: Consistency Is The Message

Finance isn’t shouting, but it is showing up.

- A clear, consistent increase from January to March 2025.

- Utilisation patterns are less volatile than in legal or services.

- Like others, it saw a dip over Christmas — but the recovery was swift.

Banking seems to be finding its hybrid groove without over-correcting. In a sector driven by compliance, routine, and risk management, a predictable return to office is aligned with operational needs and leadership preferences.

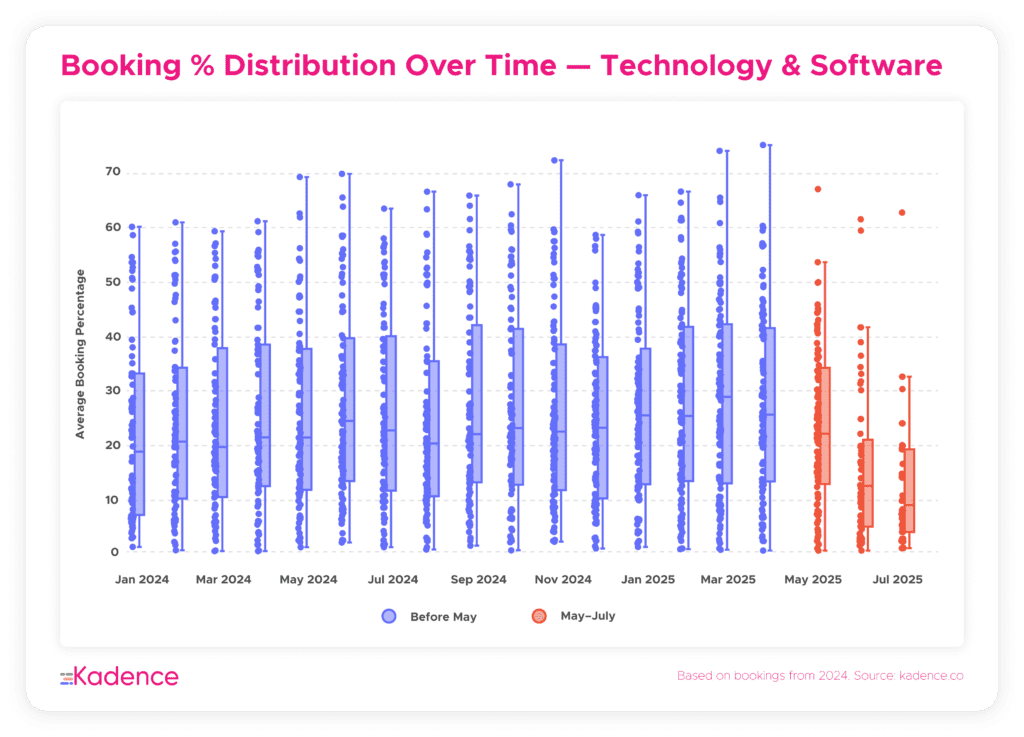

Tech & Software: Still Playing It Cool

Despite being the architects of flexible work, even technology firms are stirring.

- Average utilisation remained modest, with 50% of buildings between 15–42%.

- But from November 2024, outliers began extending upward — suggesting some teams are experimenting with more in-office time.

- The post-Christmas bounce is real, but not dramatic.

This sector is clearly still in test-and-learn mode — balancing freedom with function. While many teams are exploring office returns, deeply ingrained autonomy, distributed teams, and retention-sensitive cultures mean change is incremental and adaptive.

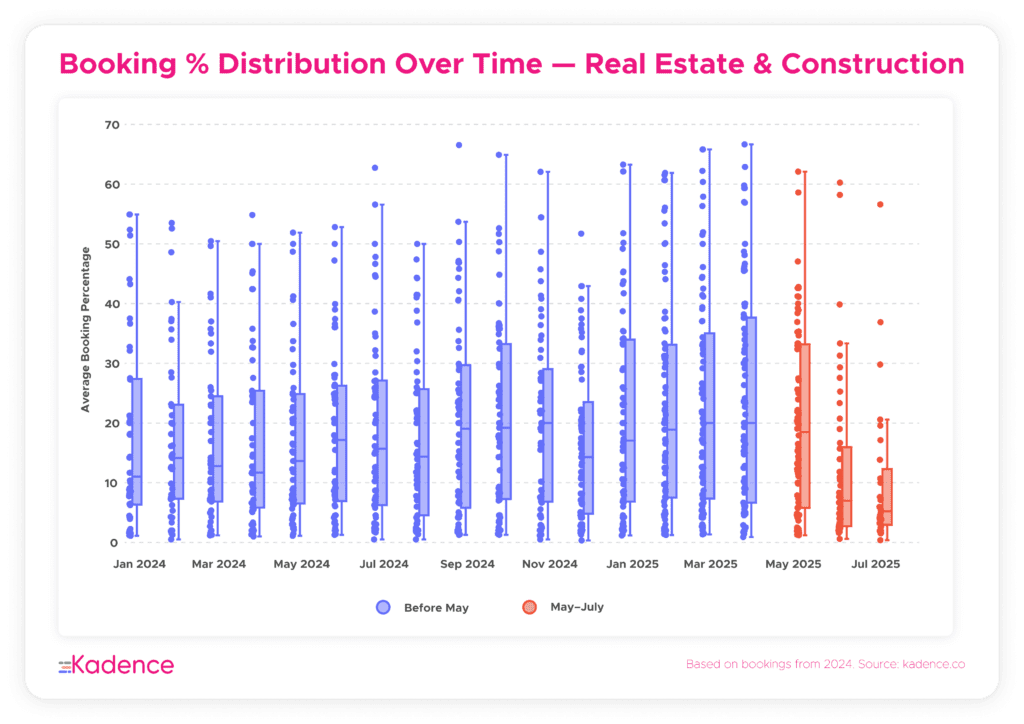

Real Estate & Construction: Mirroring Tech

Real Estate & Construction share tech’s trajectory:

- Low overall averages, with some growth into early 2025.

- Outliers appearing only recently.

- Could signal construction demand aligning with return-to-office builds, or just more boots on the ground for site-based work.

Office presence is tied less to policy and more to operational need, with field-based roles and project-based workflows dictating when, and if, people come in.

The Office Week Tells A Sharper Story

To truly understand how teams are using office space, we zoomed in on the rhythm of the week — focusing exclusively on Tuesdays, Wednesdays, and Thursdays. These “anchor days” have become the unofficial backbone of hybrid work schedules — the days when people are most likely to coordinate their in-office presence.

By filtering our dataset to include only bookings made on these midweek days, several things become clear:

- Utilisation rates are noticeably higher than the all-days average. This isn’t surprising — it reflects intentional, coordinated office attendance rather than ad hoc usage.

- The distribution curve shifts right, indicating more buildings moving into the 40–60% range and above. This is especially visible in the histogram view, where the tail of high-performing buildings becomes more pronounced.

- Sector-by-sector, we see sharper divergence in behaviour. Some industries treat these peak days as essential collaboration windows. Others, even on their busiest days, hover below the mid-30s — suggesting remote-first norms or asynchronous team structures.

To bring this to life, we overlaid smoothed trend lines for each industry. Legal, finance, and life sciences peak sharply midweek — with some buildings pushing past 70% average utilisation. Meanwhile, sectors like tech and media still prefer flexibility, showing gentler curves even on peak days.

What this tells us is critical: the return to the office isn’t random — it’s concentrated. Hybrid work is becoming not just a question of where we work, but when.

A Structural Shift Is Underway

Look across sectors, and March–April 2025 is a clear inflection point. Every industry shows a meaningful climb. This isn’t a temporary rebound. It’s a signal that hybrid is shifting from experiment to expectation.

And that means the real work — building around the rhythms that are taking hold — starts now.

Want to see how your team compares? Book a demo with our hybrid experts and discover how real-time workplace intelligence can help you plan, coordinate, and optimize your office around the moments that matter most.