Over the past three months, some of the largest enterprises in the world have quietly made a very loud statement about where they think costs need to come from. Amazon cut 16,000 corporate roles in January. Block reduced its headcount by nearly 40 percent in February. Meta is now reportedly planning reductions that could affect one in five of its 79,000 employees. For senior leaders watching this wave of layoffs, office space is the consequence nobody is talking about. The workforce shrinks in weeks. The leases do not.

The Lease Doesn't Leave When the People Do

Corporate real estate operates on a fundamentally different timescale to headcount. Workforce decisions can be made and implemented in weeks. Real estate commitments typically run for five to ten years, with break clauses that are rarely as flexible as the contracts suggest. When a company reduces its workforce by 15 or 20 percent, it does not automatically shed 15 or 20 percent of its property obligations. Those costs sit on the balance sheet, quietly compounding, long after the layoffs and office space decisions have faded from the news cycle.

This is not a theoretical risk. According to PwC’s 2026 emerging trends in real estate report, nearly half of all office leases signed before the pandemic have yet to roll over. Many of those agreements were sized for a workforce and a set of working patterns that no longer exist. National office vacancy is now sitting at around 18.6 percent and that figure reflects the market average, not the internal utilization picture inside individual enterprises, which is frequently worse.

The result is a structural mismatch that most organizations are carrying without a clear plan to address it. Headcount has been cut. Real estate has not caught up. And in many cases, leadership does not have the visibility to even understand the scale of the problem.

The RTO Collision

What makes this moment particularly complex is that workforce reductions are happening at exactly the same time as a wave of return-to-office mandates. Stellantis is requiring all US employees back five days a week from the end of this month. Ubisoft, Novo Nordisk, TikTok and dozens of others have introduced full or near-full in-office requirements in the first quarter of 2026. According to JLL, more than half of Fortune 100 companies now require five-day office attendance, a figure that stood at just 5 percent two years ago.

The instinct behind these mandates is understandable. Leaders want visibility, collaboration and cultural cohesion. But the operational reality of bringing fewer people into offices that were designed for more creates a specific kind of problem: space that looks occupied on paper but performs poorly in practice. Teams spread across floors that no longer make sense. Collaboration zones that sit empty because the teams they were built for have contracted. Real estate costs that cannot be justified against the headcount that remains.

Returning to the office and right-sizing your real estate are two different problems that most enterprises are currently treating as one. Leaders managing layoffs and office space obligations simultaneously are finding the gap between headcount decisions and property commitments wider than they expected.

What Senior Leaders Are Not Asking

When a CFO signs off on a restructuring, the conversation almost always centers on payroll savings, severance costs and the timeline to profitability. Real estate is rarely part of that initial calculation, even though for most large organizations it is the second-biggest cost on the balance sheet after people.

The questions that should be asked, and often are not, include: which floors, buildings or locations are now structurally oversized relative to the teams that remain? Which leases are approaching break clauses or expiry points where a different decision can be made? How is actual space utilization changing as attendance patterns shift post-restructuring? And what does the right footprint look like in 18 months, not for the headcount that existed when the lease was signed, but for the organization that exists today?

Without reliable answers to those questions, real estate decisions default to inertia. Companies hold space they do not need because nobody has made the case, with data, to do otherwise.

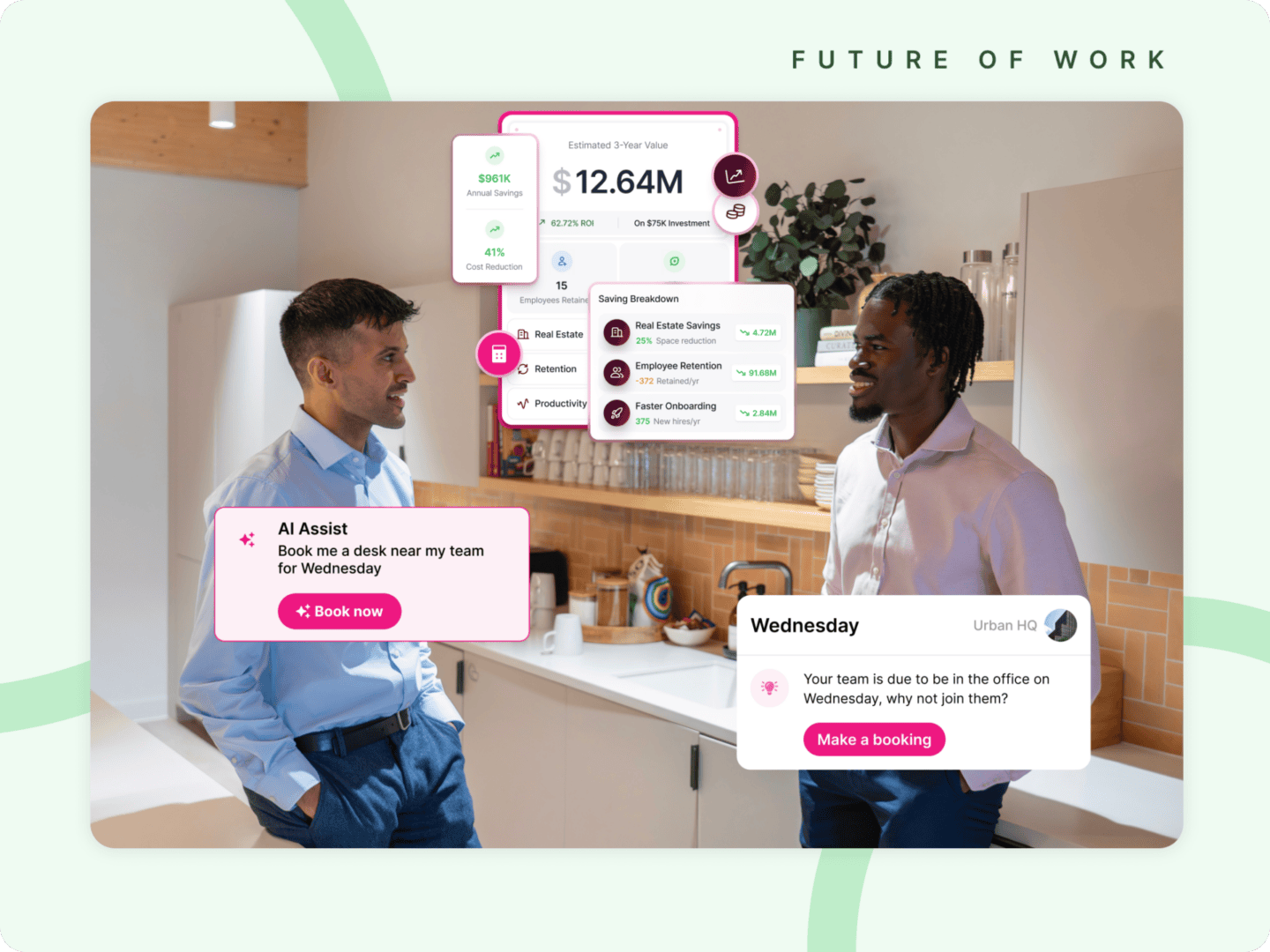

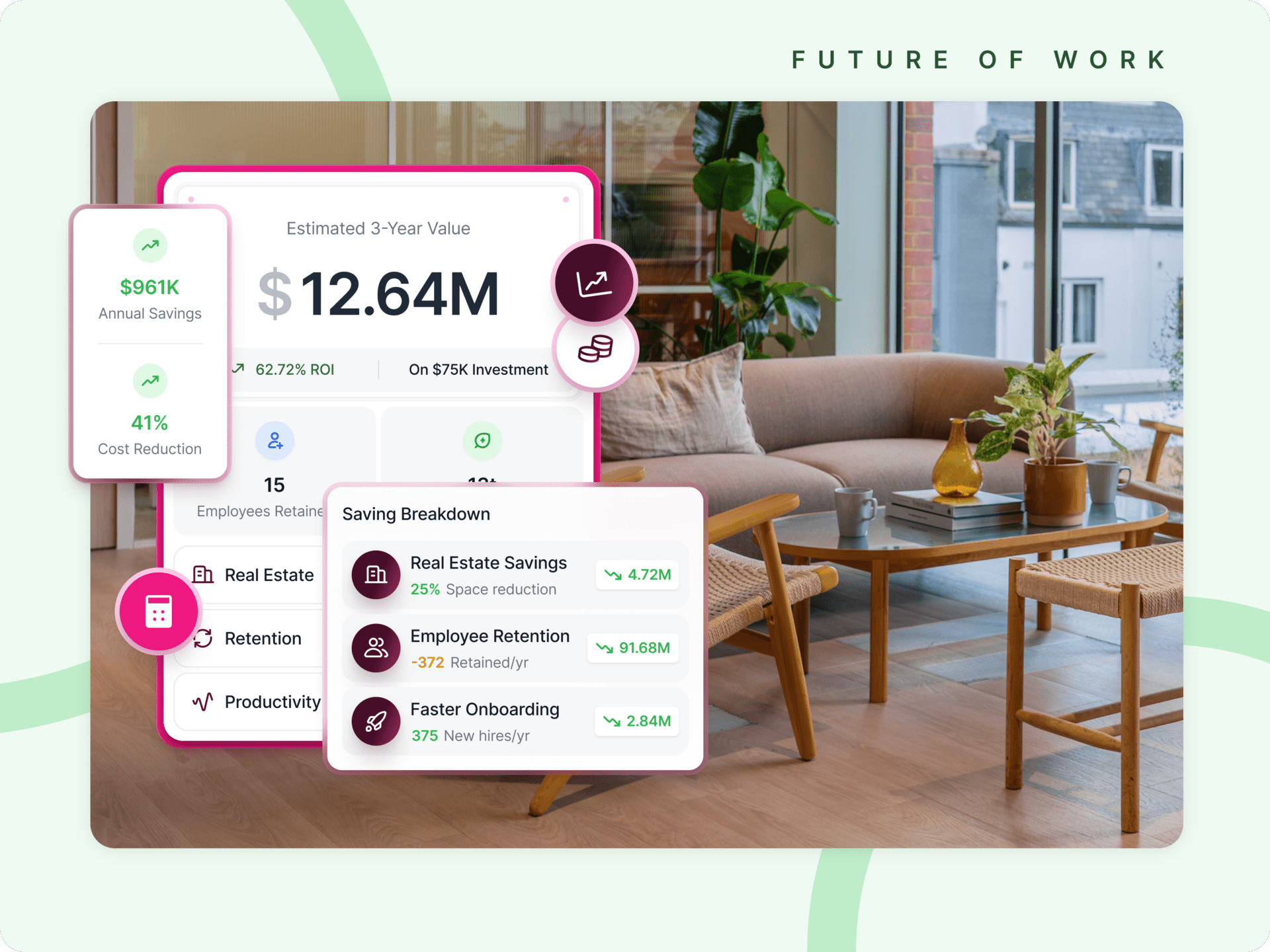

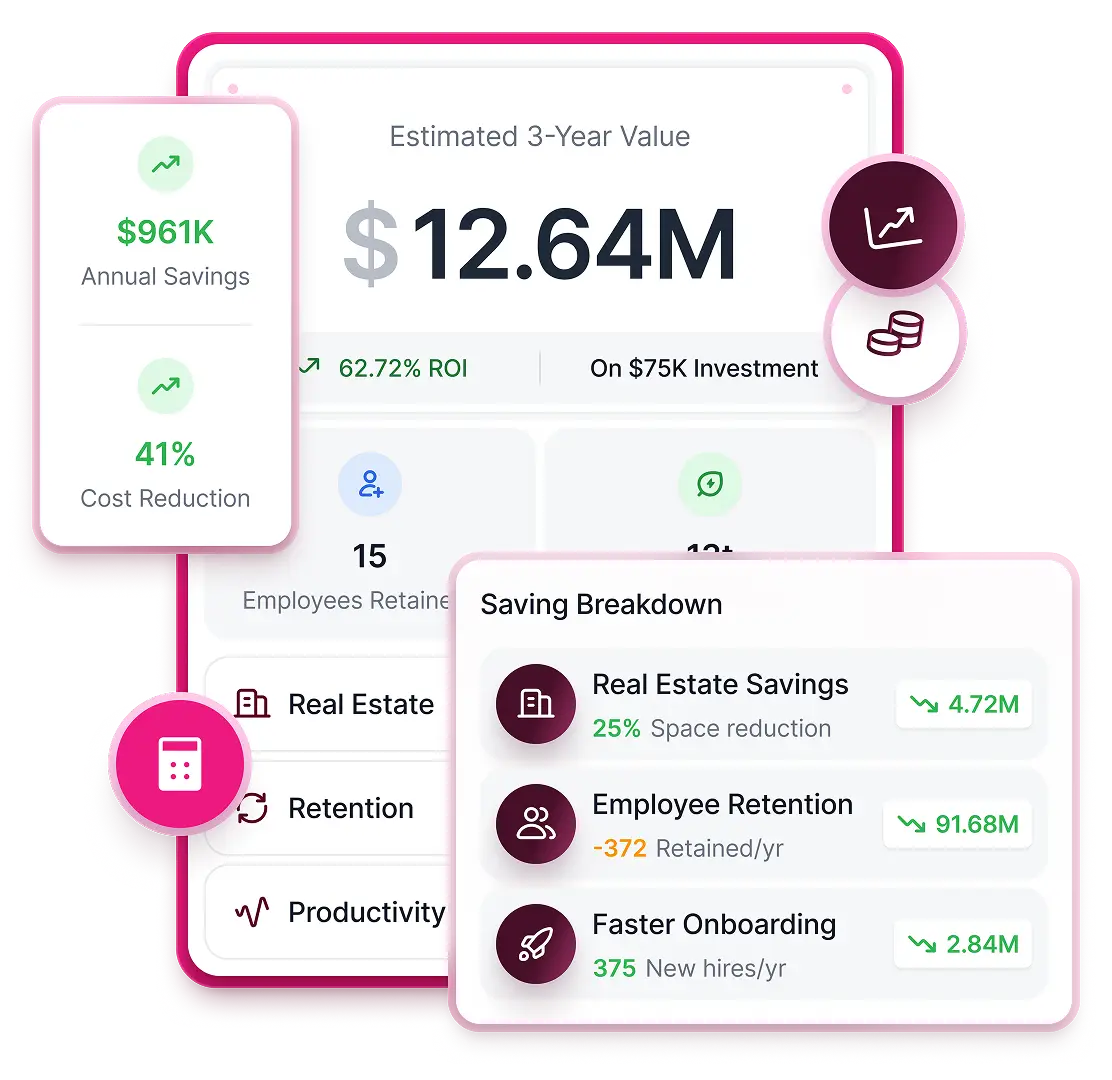

Calculate the ROI of Your Workplace Operations

Our brand-new ROI Calculator is here to help you visualize your success in seconds.

The Cost of Carrying Dead Space

The financial exposure is significant and often under-appreciated at board level. McKinsey research shows that 40 percent of office space goes unused on a typical workday and that was before this year’s wave of reductions. With average US office costs running at around $37 per square foot, a large enterprise carrying even a modest amount of surplus space after a restructuring can be paying millions annually for square footage that serves no operational purpose.

This is not purely a cost issue, though the cost is real and material. It is also a strategic one. Capital tied up in unnecessary real estate is capital that cannot be deployed elsewhere. It signals to investors and analysts that operational discipline has not extended to the full cost base. And it creates a physical environment that feels underused, which has its own effect on the culture and energy that the return-to-office mandate was supposed to restore.

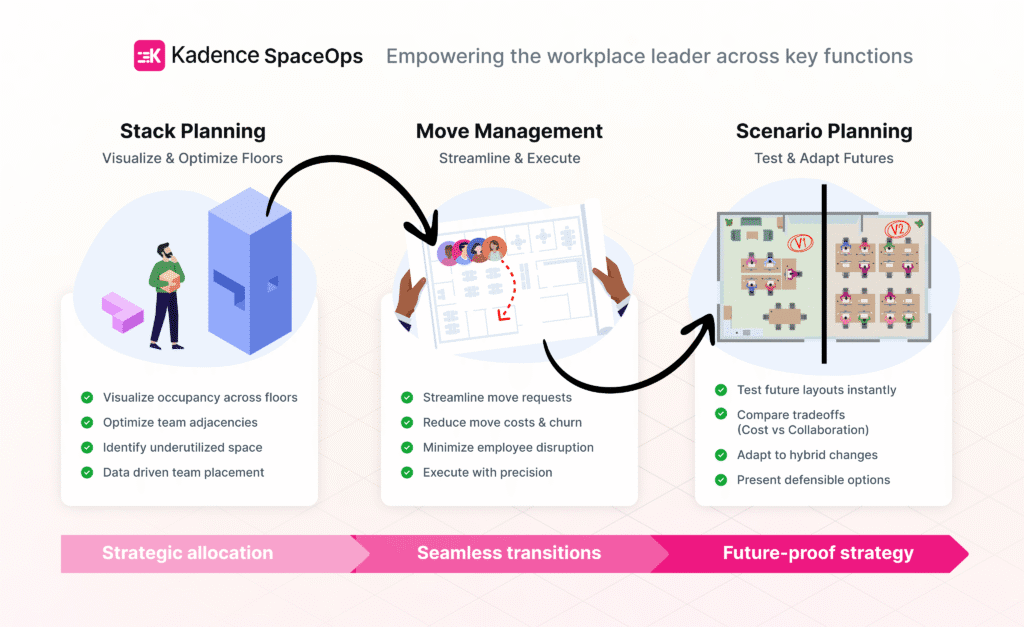

SpaceOps Turns a Liability Into a Decision

The organizations that will navigate this transition most effectively are not the ones that cut headcount fastest or mandate the most aggressive return policies. They are the ones that treat their physical estate as an active, data-driven asset rather than a fixed cost.

That is what SpaceOps makes possible. Rather than managing real estate as static square footage against a historical headcount, a SpaceOps approach gives senior leaders continuous visibility into how space is actually being used. Which teams are present and when. Which areas are generating genuine collaboration. Which buildings are performing against their cost and which are not. When that data is connected to workforce planning, it becomes possible to make proactive decisions about consolidation, reconfiguration and renegotiation, rather than reactive ones triggered by the next restructuring cycle.

Practically, this means being able to answer questions that most organizations currently cannot. If we reduce headcount in this division by 20 percent, what is the actual impact on our space requirement in this building? If we mandate four days in the office, which floors will genuinely be utilized and which will sit half-empty? If this lease expires in 18 months, what does our footprint need to look like to reflect the organization we are today, not the one we were when we signed?

The companies building this capability now will enter the next restructuring cycle with a material advantage. They will move faster, justify decisions with evidence, and avoid carrying the kind of real estate liability that is currently sitting, largely unexamined, across some of the world’s largest organizations. For any business working through layoffs and office space decisions in parallel, that capability is increasingly the difference between a restructuring that genuinely reduces cost and one that simply moves it somewhere less visible.

The Strategic Imperative

The headlines from this wave of workforce reductions will move on. The real estate obligations will not.

For senior leaders overseeing large physical estates, the question right now is whether the organization has the operational intelligence to understand what those obligations actually look like relative to the workforce that remains. In most cases, the honest answer is that it does not, not with the granularity or the currency that this moment requires. The connection between layoffs and office space has to become part of how restructuring decisions get made, not an afterthought that surfaces six months later when the balance sheet tells the story.

McKinsey projects that office demand could be 20 percent lower by 2030 in major cities. The pace of workforce change in 2026 is accelerating that shift inside individual organizations right now. Enterprises that build the capability to connect people data to space data, and space data to financial decisions, will be better positioned to manage costs, move faster, and turn their physical estate into something that actively supports performance rather than quietly draining it.

If you are reassessing your real estate strategy in the context of recent or planned workforce changes, speak to our workplace operations team to see how Kadence helps enterprises build the SpaceOps capability to make smarter, faster decisions about their physical estate.